.svg)

.png)

This topic has made headline after headline over the last year and most notably in the last few months as oil reaches 2021 levels. But how can that be, the war is still ongoing and OPEC+ is trying to add fuel to the flames. All the signs point to higher oil prices. But this is our reality.

The price of oil isn’t affected any differently than any other real or intangible asset. It is influenced by supply and demand.

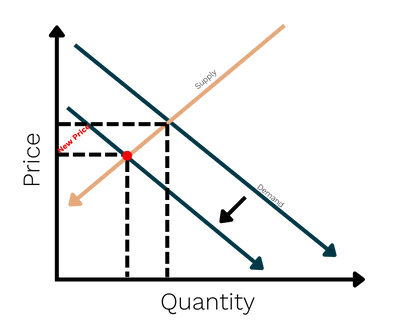

When you take out some supply (change in supply) you will shift the supply curve to the left thus increasing the price and changing the amount of quantity demanded.

You can see the relationship, as you have less supply you will have higher prices if demand stays the same. But what about if demand changes?

Recession changes demand, China ranks second in the world for oil consumption, accounting for about 13.2% of the world's total consumption.

China is facing hardships as companies are leaving to diversify and secure their supply chains, which will reduce global demand for oil. In other parts of the world where supply chains are being diversified too oil and gas may not be as important as a source of energy, they may get more energy from coal, solar, wind, nuclear, etc. That will reduce and change the demand for oil.

In this chart, I am going to leave the supply changed, because that is the environment we are living in. Russia has changed the supply of oil and gas available to the world.

When global demand changes, and namely falls, the price will fall with it, and the quantity supplied changes.

There’s more to what meets the eye with these charts but without getting a bachelor’s in economics, this will suffice.

The charts can have different slopes, be concave, be moving simultaneously, and they are almost always, in some sense, backward looking.

Now back to the price of oil.

Here’s a brief recap of 2022 supply and demand changes.

That is how we have lower oil prices. It is simply a change in the supply and demand for oil. Recession causes manufacturing to decrease which needs oil.

There is precedence for production cuts to drastically increase the price of oil and gas.

“The embargo ceased U.S. oil imports from participating OAPEC nations, and began a series of production cuts that altered the world price of oil. These cuts nearly quadrupled the price of oil from $2.90 a barrel before the embargo to $11.65 a barrel in January 1974” - Michael Corbett, Federal Reserve Bank of Boston

Sanctions are what sent the price of oil and gas skyrocketing in 2022. In opposition of Russia’s invasion of Ukraine, developed economies stopped companies from buying Russian energy. That took about 12% of the world’s production out of circulation. And of course, we all know what followed.

In the 70s it was the OPEC oil embargo that sent prices skyrocketing. An important distinction to make is that OPEC produced the oil for the world in the 70s, today oil production is much more diversified and the US is a net exporter of energy.

A supply shock today, like in the 70s, would not likely cause as much harm to price because there is less reliance on any one organization or country for the production of oil.

Although we are already 12% short and more production cuts would further damage that situation. But demand is continually falling.

So here is the situation.

If the Federal Reserve achieves a soft landing and we have no recession I think we could see a sharp climb in oil prices once again because perceived demand at the very least would be higher, if not actual demand.

If we hit a harder recession then the price of oil and gas would fall more or at least not rise. Even with production cuts, the falling demand would be enough to neutralize it.

Overall I see a lot of volatility in the next 12 months in the price of oil because of these 2 factors, supply and demand in the wake of a global recession.

It’s not commodity funds. I really think that energy companies are poised to take more advantage of energy volatility, and here’s why.

We are already starting to see that happen as well. Energy companies are capitalizing on higher energy prices earlier in the year, returning cash to shareholders, and institutions are back to buying.

It is hard to say if energy companies will continue to outperform but there is some room for performance from here. Of course, there is always opportunity costs to doing this, because maybe it won’t outperform everything from here.